18 July 2026 · 13 min read

Monthly Household Expenses List: What to Include in a Family Budget

A family budget is easier to build when you know exactly what needs to go into it. A good monthly household expenses list helps you see the full pattern before you set category caps.

The problem is that household spending rarely arrives in one neat list. Rent or mortgage payments are obvious, and groceries are easy to remember. But subscriptions, school costs, parking, medicine, birthday gifts, repairs, pet care, and annual renewals can quietly distort your monthly picture if they aren’t accounted for.

A good monthly household expenses list helps you see the full pattern before you set category caps.

This guide breaks household expenses into practical groups: fixed monthly costs, variable everyday spending, child-related expenses, irregular costs, and commonly forgotten items. Use it as a checklist when building or reviewing your family budget.

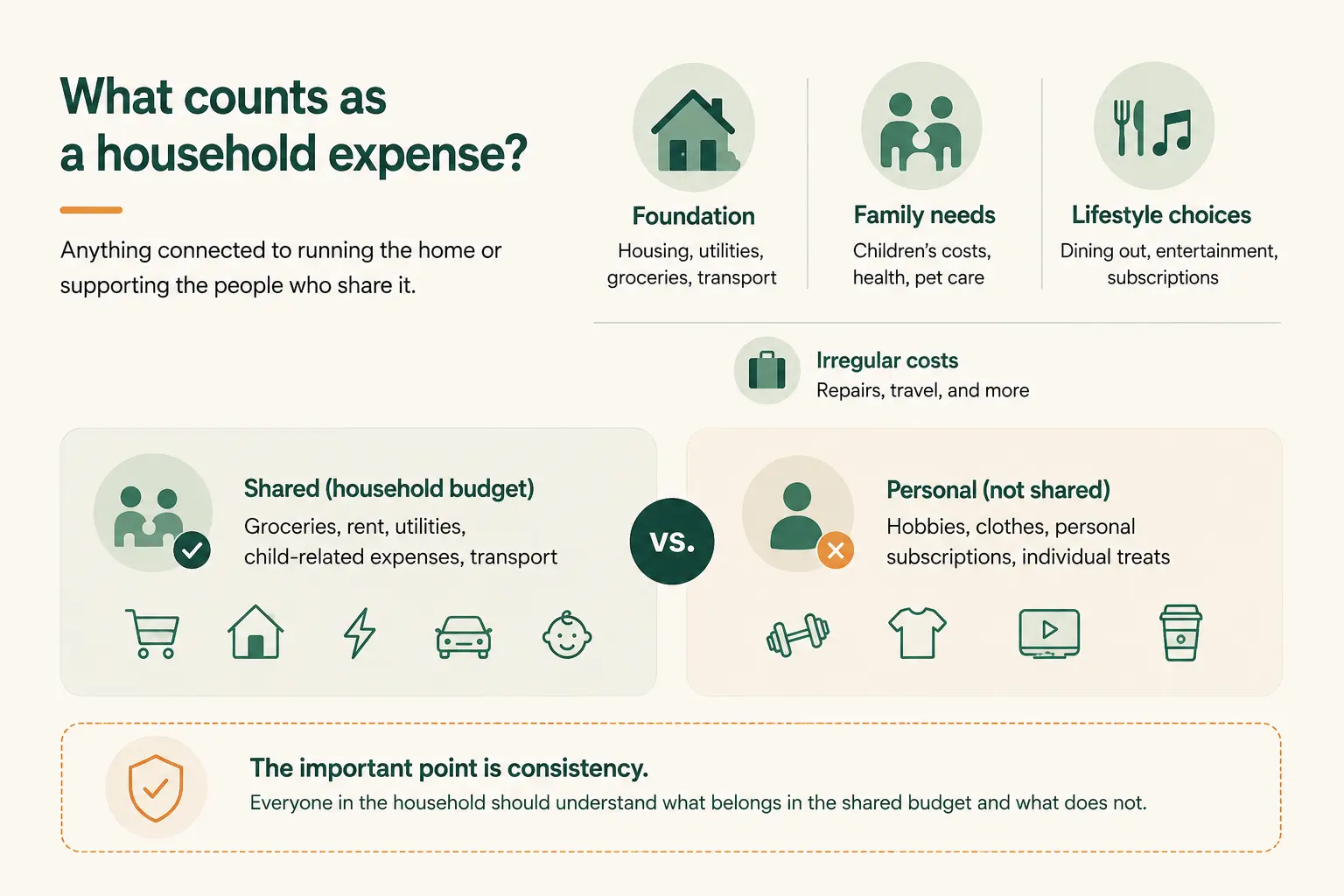

What counts as a household expense?

A household expense is any cost connected to running the home or supporting the people who share it. That may include your foundation (housing, utilities, groceries, and transport), family needs (children’s costs, health, and pet care), and lifestyle choices (dining out, entertainment, and subscriptions), along with irregular costs like repairs or travel.

Not every expense needs to be shared. A couple or family may decide that some costs belong in the household budget while others remain personal. For example, the shared budget may include groceries, rent, utilities, and child-related expenses, while personal hobbies, clothes, or individual subscriptions remain separate.

The important point is consistency. Everyone in the household should understand what belongs in the shared budget and what does not.

Fixed monthly household expenses

Fixed expenses are costs that appear regularly and are usually predictable. They should be entered first because they use part of the monthly budget before everyday spending begins.

Housing

Housing is often the largest household expense. This includes your rent or mortgage payment, property management fees, service charges, building maintenance, property tax (if paid monthly), HOA fees, and any storage or parking space rentals. If housing costs are paid annually or quarterly, divide the amount into a monthly equivalent so the budget reflects the true ongoing cost.

Utilities

Utilities cover the basic services needed to run the home, such as electricity, gas, water, heating, waste collection, internet, mobile phone plans, and TV licences or cable services. Some utility bills are stable, while others change by season. Heating and electricity may require higher caps during winter or summer, depending on your home.

Insurance

Insurance payments may be monthly, quarterly, or annual. Remember to account for home or renters insurance, car insurance, health and life insurance, pet insurance, and protection plans for devices or appliances. If a policy is paid once or twice a year, include a monthly allowance in the budget rather than treating the payment as a surprise.

Debt and loan payments

If debt payments are part of the household’s regular obligations, include them clearly. This covers car loans, personal or student loans, credit-card repayments, and financing for appliances or furniture. Do not mix debt repayment with everyday spending categories; it is easier to understand the budget when obligations and flexible spending are separated.

Childcare and education

Some child-related expenses are fixed enough to include at the start of the month. This includes nursery or daycare fees, school tuition, after-school care, tutoring, school meals, and regular paid clubs, sports, or music lessons. If these costs are predictable, treat them like fixed expenses rather than waiting to record them as they happen.

Subscriptions and memberships

Subscriptions are easy to forget because they often renew automatically. Check your accounts for streaming services, cloud storage, news subscriptions, fitness memberships, software, gaming, children’s learning apps, and delivery memberships. Review this category every few months. A small subscription may not seem important on its own, but several recurring payments can become a meaningful monthly cost.

Variable monthly household expenses

Variable expenses change from month to month. These are the categories that most often need active tracking.

Groceries

Groceries usually include food and basic items bought for use at home, such as supermarket purchases, food markets, bakery items, drinking water, baby food, and snacks. Decide whether cleaning products, toiletries, and pet food belong under groceries or separate categories. Both approaches can work, provided the household applies the same rule every month.

Household supplies

This category covers products used to maintain the home: cleaning products, laundry detergent, dishwashing products, toilet paper, batteries, light bulbs, kitchen supplies, small tools, and replacement items. Some supermarket receipts may need to be split between groceries and household supplies, but that split is useful only if the household wants to control those costs separately.

Transport

Transport includes daily movement and commuting costs. Factor in fuel, public transport, taxis, ride-hailing services, parking, tolls, train and bus tickets, and routine car washes or bike maintenance. Car repairs and annual insurance may be better placed in a separate car category if they are large or irregular.

Dining out

Dining out should usually be separate from groceries because it reflects a different spending decision. This includes restaurants, cafés, takeaway meals, food delivery, work lunches, and coffee shops. This category is often one of the easiest to adjust when the household needs to reduce flexible spending.

Health and pharmacy

Health expenses may be predictable or irregular. Include doctor and dentist visits, prescriptions, over-the-counter medication, vitamins, physiotherapy, therapy, glasses, contact lenses, medical tests, and first-aid supplies. If health expenses vary significantly, keep a buffer in the monthly budget.

Personal care

Personal care can be shared or personal depending on the household’s rules. It covers haircuts, skincare, cosmetics, toiletries, hygiene products, and salon visits. Families may choose to include children’s personal care in a children’s category instead.

Clothing and shoes

Clothing can be regular, seasonal, or occasional. Include adult and children’s clothing, shoes, coats, school uniforms, sports clothing, work attire, and tailoring. If clothing costs are irregular, a monthly cap can help prevent seasonal purchases from disrupting the budget.

Children

A children’s category gives the household a clear view of child-related spending. This groups together school supplies, toys, books, clothes, activities, school trips, birthday parties, sports equipment, pocket money, and children’s medical costs. Some families prefer to split this into education, activities, clothing, and childcare, while others prefer one broad children category.

Pets

Pet expenses can be predictable and irregular, covering pet food, veterinary care, medication, grooming, insurance, toys, accessories, and boarding or pet sitting. Because veterinary bills can be large, pet care may need a monthly buffer or a separate emergency allowance.

Entertainment

Entertainment covers shared leisure spending, such as cinema tickets, events, concerts, museums, family activities, games, paid attractions, and sports events. Streaming services can go here or under subscriptions — just choose one approach and apply it consistently.

Gifts and celebrations

Gifts are often forgotten until the month becomes expensive. Include birthday and holiday gifts, party supplies, cards, flowers, decorations, family celebrations, and teacher or wedding gifts. This category is especially useful for families with children because school and birthday events can appear frequently.

Travel and trips

Travel can be monthly, seasonal, or occasional. It includes flights, train tickets, hotels, car hire, travel insurance, fuel for trips, meals during travel, tourist attractions, and luggage. For occasional trips, keep travel separate from daily transport so the monthly budget remains easy to understand.

Irregular household expenses people often forget

Not every household expense happens every month. These costs still belong in the budget because they affect the household’s spending capacity.

Annual and semi-annual payments

To avoid surprises with insurance renewals, car registration, annual subscriptions, school fees, software renewals, or professional licences, divide the annual cost by 12 and include a monthly allowance.

| Example | Annual cost | Monthly allowance |

|---|---|---|

| Car insurance | $1,200 | $100 |

| School supplies fund | $600 | $50 |

| Annual subscriptions | $240 | $20 |

| Gifts and holidays | $1,200 | $100 |

Home repairs and maintenance

These expenses do not happen every month, but plumbing, electrical, or appliance repairs, furniture replacement, paint, garden maintenance, and pest control are an inevitable part of running a household.

Car repairs and maintenance

A household with a car should usually include a monthly car-maintenance allowance for tyres, oil changes, brake repairs, inspections, battery replacement, and emergency repairs, even if no repair is expected this month.

Medical and dental surprises

A health buffer can prevent an emergency dental treatment, specialist appointment, prescription change, or glasses replacement from breaking the monthly plan.

Seasonal costs

Seasonal costs are predictable when viewed across the year, even if they do not appear every month. Factor in winter clothing, summer camps, holiday travel, heating or air-conditioning increases, back-to-school shopping, and seasonal home maintenance.

Monthly household expenses checklist

Use this checklist to prepare your family budget checklist.

| Expense group | Examples | Include in budget? |

|---|---|---|

| Housing | Rent, mortgage, property fees | Yes / No |

| Utilities | Electricity, gas, water, internet | Yes / No |

| Insurance | Home, car, health, pet | Yes / No |

| Debt payments | Loans, credit cards, financing | Yes / No |

| Groceries | Food and regular supermarket purchases | Yes / No |

| Household supplies | Cleaning, laundry, paper goods | Yes / No |

| Transport | Fuel, public transport, parking, taxis | Yes / No |

| Children | School, childcare, activities, clothes | Yes / No |

| Health | Doctor, dentist, medicine, glasses | Yes / No |

| Personal care | Haircuts, toiletries, cosmetics | Yes / No |

| Clothing | Clothes, shoes, uniforms | Yes / No |

| Pets | Food, vet, grooming, insurance | Yes / No |

| Dining out | Restaurants, cafés, takeaway | Yes / No |

| Entertainment | Events, games, family activities | Yes / No |

| Subscriptions | Streaming, apps, memberships | Yes / No |

| Gifts | Birthdays, holidays, celebrations | Yes / No |

| Travel | Trips, hotels, flights, activities | Yes / No |

| Repairs | Home, car, appliance repairs | Yes / No |

| Buffer | Irregular or unexpected expenses | Yes / No |

How to group household expenses into budget categories

After listing expenses, group them into categories that are simple enough to use every day. Avoid creating too many categories at the start; a budget with eight to twelve main categories is usually easier to maintain than one with fifty. A category should only exist when it supports a real household decision.

| Category | What it includes |

|---|---|

| Housing | Rent, mortgage, property fees |

| Utilities | Electricity, gas, water, internet |

| Groceries | Food and everyday supermarket purchases |

| Transport | Fuel, public transport, parking, taxis |

| Children | School, childcare, activities |

| Health | Medicine, doctor, dentist, glasses |

| Household | Cleaning products, repairs, home items |

| Dining out | Restaurants, cafés, takeaway |

| Subscriptions | Streaming, apps, memberships |

| Clothing | Clothes, shoes, uniforms |

| Gifts | Birthdays, holidays, celebrations |

| Other | Rare expenses that do not fit elsewhere |

How to set a monthly cap for each expense category

Once the categories are clear, assign a monthly cap to each one.

Step 1: Start with the overall household spending cap

Choose the total amount the household plans to spend during the month (e.g., $4,000). This number should cover only the expenses included in the household budget.

Step 2: Add fixed expenses first

Start with costs that are predictable or difficult to change. If rent is $1,500, utilities are $300, insurance is $180, internet is $120, childcare is $400, and subscriptions are $80, your fixed expenses total $2,580. This leaves you with $1,420 for variable spending.

Step 3: Allocate variable categories

Distribute the remaining amount across your variable categories like groceries ($650), transport ($250), health ($100), household ($120), dining out ($150), entertainment ($80), and gifts ($50).

Step 4: Keep a visible buffer

A budget does not need to allocate every dollar immediately. A buffer helps with higher grocery costs, unexpected school expenses, small repairs, or forgotten renewals. CapKin makes this easy by letting you set an overall cap and category limits, keeping any leftover funds visible as a “To Be Allocated” buffer. It focuses purely on tracking what you spend, without connecting to your bank or complicating things with net-worth tracking.

Fixed vs variable expenses: why the difference matters

Fixed and variable expenses require different behaviour. Fixed expenses (like rent, insurance, childcare, and subscriptions) need planning because they often happen automatically. If they are not added at the start of the month, the household may think more money is available than it really is.

Variable expenses (like groceries, transport, dining out, and gifts) need tracking because they change depending on daily choices and events. A monthly budget works best when fixed costs are planned first and variable costs are tracked throughout the month.

Should savings be included in monthly household expenses?

Savings are important, but they are not the same as expenses. An expense is money spent on something; savings are money set aside.

Some households include savings as a budget line because they want to treat it as a non-negotiable monthly commitment. Others manage savings separately and keep the household budget focused only on spending. For a shared expense tracker, it is usually clearer to separate your spending plan (what you expect to spend) from your savings plan (what you want to set aside).

To keep things simple, CapKin deliberately focuses on your shared spending rather than acting as a complex wealth management tool. By separating your spending from your savings, you get a much clearer picture of your daily habits.

How to handle mixed purchases

Some purchases contain items from several categories. If a supermarket receipt contains groceries, cleaning spray, a school notebook, and birthday candles, you can handle it in three ways.

- Option 1: Record the full amount under the main category. Use this when most of the purchase clearly belongs to one category (e.g., Supermarket — $86 — Groceries). It is the fastest method.

- Option 2: Split the purchase by category. Manually divide the receipt into Groceries ($62), Household ($12), Children ($8), and Gifts ($4). This is more accurate but takes more time.

- Option 3: Speak or type the split immediately. Simply say, “Groceries 62, cleaning products 12, school notebook 8 and birthday candles 4.” CapKin is designed exactly for this type of entry: household members can say what they bought, the app sorts it into line items and categories, and uncertain items require confirmation before saving.

Monthly household expenses example

Here is a sample family budget using a $4,000 monthly household spending cap.

| Category | Monthly cap |

|---|---|

| Housing | $1,500 |

| Utilities | $300 |

| Insurance | $180 |

| Internet and phones | $120 |

| Childcare and school | $400 |

| Groceries | $650 |

| Transport | $250 |

| Health | $100 |

| Household | $120 |

| Dining out | $150 |

| Entertainment | $80 |

| Subscriptions | $80 |

| Gifts | $50 |

| To Be Allocated / buffer | $20 |

| Total | $4,000 |

This is only an example. A household with no children, a lower rent payment, or higher transport costs would need a different structure. The purpose is not to copy another family’s numbers, but to create a complete list, group it into useful categories, and set realistic caps.

Common household expenses that are easy to miss

Review this list before finalising the budget to catch the small leaks. On the road, you might forget parking, tolls, car servicing, or public transport top-ups. Around the house, watch out for printer ink, batteries, light bulbs, app subscriptions, replacement chargers, or laundry costs. Finally, don’t forget occasional social and personal costs like birthday gifts, school trips, work lunches, pharmacy purchases, or taking the dog to the vet for medication. Many of these are small individually, but together, they can explain why a monthly budget feels inaccurate.

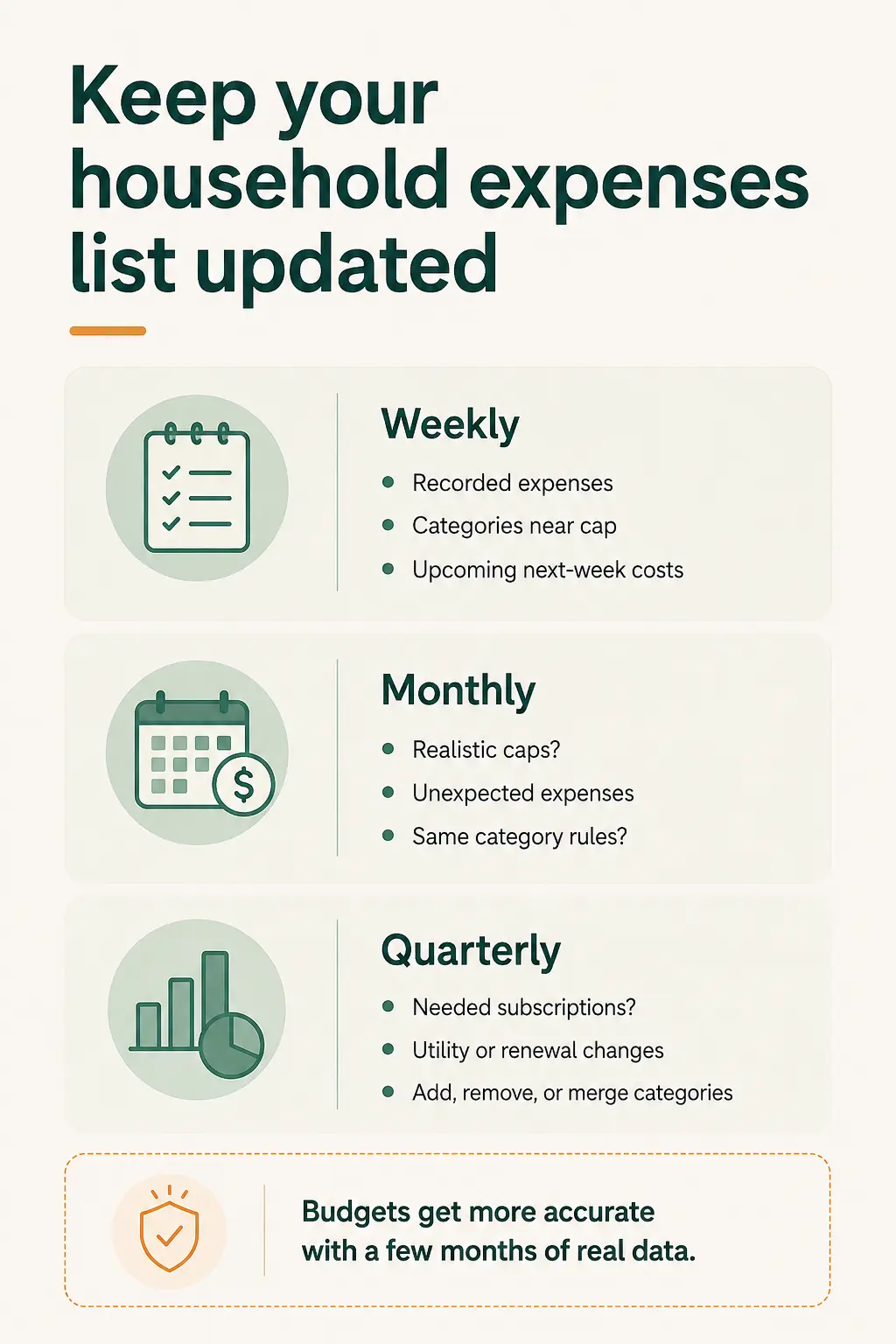

How to keep the household expenses list updated

A household expenses list is not a one-time document. Review it regularly using these intervals:

Weekly review: Check which expenses were recorded, which categories are close to their caps, and if anyone forgot to log purchases. Look ahead to see if any child-related or household costs are pending next week.

Monthly review: Check which categories were realistic and which caps were too low or too high. Discuss which expenses appeared unexpectedly, if the buffer was large enough, and if the household used the same category rules.

Quarterly review: Ask if subscriptions are still needed, if utility costs changed, or if annual renewals are approaching. Decide if any category should be added, removed, or merged. A budget becomes more accurate after a few months of real data.

How a shared tracker makes household expenses easier to manage

The hardest part of a household budget is not usually the first setup; it is keeping the budget current. If one person records every purchase, the system becomes fragile. If everyone has a simple way to contribute, the picture becomes more reliable.

Household spending is shared in real life: one person buys groceries, another pays for parking, a teenager picks up school supplies, and fixed costs appear at the beginning of the month. A useful budget needs to capture all of that without turning one person into the household accountant.

CapKin is built specifically for this reality: everyone in the household can say or type what they bought, the app sorts it out, keeps every category visible against its cap, and only nudges you when something needs attention.

Turn the list into a budget your household can use

A monthly household expenses list gives you the raw material for a family budget. Start with fixed costs, add variable spending, and include irregular expenses. Group everything into simple categories, then set one cap for each category and keep a small buffer for the expenses that do not fit neatly into the plan.

The final budget should be clear enough for everyone in the household to understand and simple enough to update throughout the month. CapKin is built for that everyday use: a shared household budget, spoken or typed expense capture, category caps, and human confirmation before entries affect the totals.

Every category, under its cap.

Frequently asked questions

- What are the most common monthly household expenses?

- The most common monthly household expenses include housing, utilities, groceries, transport, insurance, childcare, health costs, subscriptions, household supplies, dining out, and entertainment.

- What should be included in a family budget?

- A family budget should include all expenses the household has agreed to track. This usually means shared housing costs, food, bills, transport, child-related spending, household supplies, and recurring payments.

- How many expense categories should a household budget have?

- Most households can start with eight to twelve main categories. Add more only when the extra detail supports a useful decision.

- Should groceries and household supplies be separate?

- They can be separate if the household wants to understand food spending separately from cleaning products and home supplies. If simplicity matters more, they can be combined.

- Should personal spending be included in a family budget?

- Only if the household agrees. Some families include personal spending in the shared budget; others track only shared expenses and leave personal purchases outside it.

- How do I budget for annual expenses?

- Divide the annual amount by 12 and include that amount in the monthly budget. This works for insurance renewals, subscriptions, school expenses, holiday gifts, and other predictable costs.

- What is a household budget buffer?

- A buffer is money not assigned to a specific category. It helps cover irregular, forgotten, or higher-than-expected expenses during the month.

- What if my category caps exceed my monthly budget?

- Reduce the category caps or increase the overall spending cap. A realistic budget should not allocate more than the household plans to spend.